Global agricultural commodity markets concluded the week under a cautiously defensive trading environment, as participants reassessed global demand expectations, weather-related production risks, and the broader implications of geopolitical uncertainty on agricultural trade flows. Physical market activity across major export corridors remained active but selective, with buyers increasingly adopting short-cycle procurement strategies amid heightened pricing volatility and tighter financing conditions across portions of the commodity supply chain.

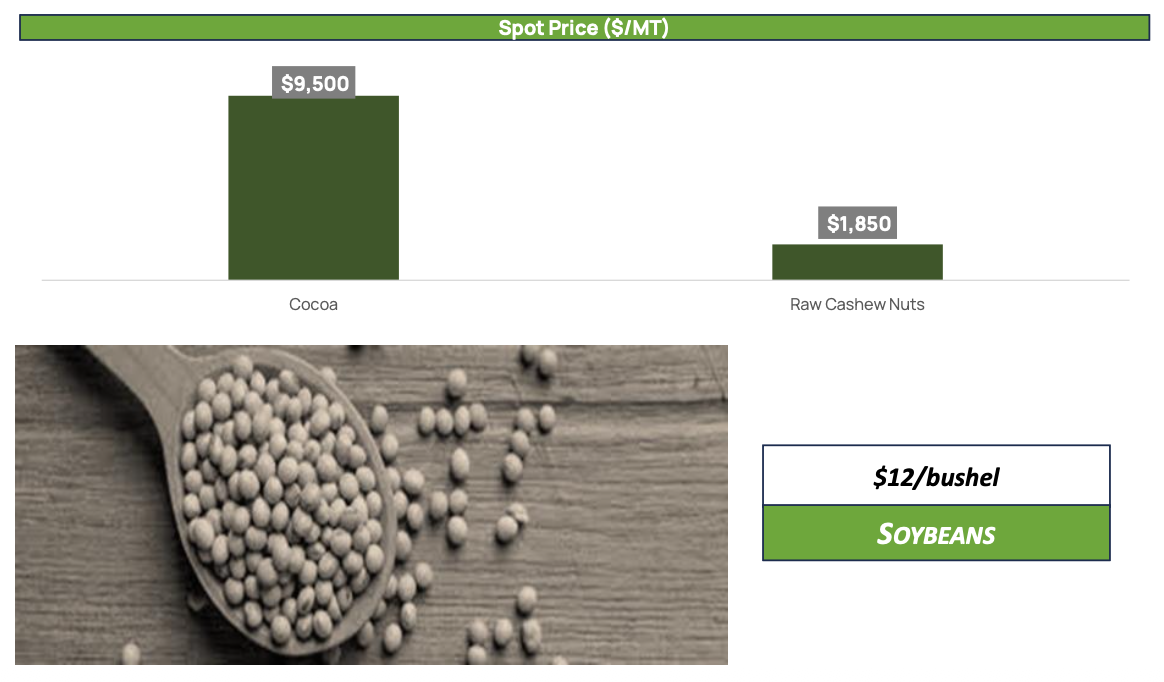

Within the oilseed complex, Soybeans experienced downward pressure after failing to sustain the momentum from recent multi-year highs. Prices retreated toward the $12/bushel region following uncertainty surrounding proposed U.S.–China agricultural purchase commitments. Market optimism had initially strengthened after discussions between President Donald Trump and President Xi Jinping fueled expectations of expanded Chinese purchases of U.S. agricultural commodities. However, sentiment weakened after Chinese authorities stopped short of confirming the proposed US$17 billion annual agricultural import target referenced by the White House.

The reversal triggered renewed caution across global soybean markets, particularly as traders reassessed export demand assumptions ahead of upcoming U.S. planting and shipment data releases. At the same time, the market continued to contend with elevated fertilizer costs, rising operational expenses, and persistent tariff-related uncertainty, all of which continued to pressure producer margins across key growing regions. Brazil also maintained a dominant position within global soybean export flows, with competitive pricing and strong harvest availability continuing to attract Asian demand away from U.S. origin cargoes.

Across the soft commodities segment, Cocoa remained one of the most closely monitored agricultural markets globally, with volatility continuing to define market behaviour despite periods of technical correction. Prices remained historically elevated as structural supply concerns across West Africa continued to overshadow temporary bouts of profit-taking. Traders remained highly sensitive to production developments across Côte d’Ivoire and Ghana, where irregular rainfall patterns, disease pressures, ageing plantations, and tightening input availability continued to threaten medium-term supply stability.

Attention also remained focused on the lingering effects of the El Niño weather cycle, which previously disrupted rainfall consistency across several cocoa-growing regions and contributed to weaker harvest quality over prior production cycles. Although weather conditions showed signs of partial stabilization during the week, market participants continued to price in climate-related production risk premiums amid concerns surrounding long-term crop sustainability and lower global stock availability.

Meanwhile, reports suggesting that Côte d’Ivoire could record a moderate recovery in cocoa output during the 2025/26 season provided some temporary relief to bearish supply concerns. Nevertheless, traders remained cautious, as broader structural deficits across the cocoa market have yet to fully normalize despite expectations of improved farmer investment and better agronomic management practices following the sustained rally in cocoa prices over the past year.

Raw Cashew Nut (RCN) markets maintained comparatively stable pricing conditions during the review period, supported by resilient procurement demand from India and Vietnam, which continue to dominate global cashew processing activity. Physical trading activity across West African export corridors remained firm, with buyers actively securing inventories amid concerns surrounding tightening origin supply and elevated inland logistics costs.

Additionally, exporters continued to navigate currency volatility, shipment scheduling delays, and tighter working capital conditions across portions of the agricultural trade finance market. Despite moderate liquidity across some physical trading channels, underlying demand fundamentals remained supportive as Asian processors continued to secure raw material inventories ahead of future export commitments and seasonal processing cycles.

Across the broader agricultural landscape, market participants continued to monitor freight market volatility, global inflation trends, geopolitical developments, and shifting trade policy expectations. Financing conditions also remained a central focus, particularly as elevated interest rates and tighter liquidity conditions continued to influence inventory financing structures, procurement timing, and overall trade execution strategies across agricultural supply chains.

Overall, the week reflected a market environment increasingly driven by macroeconomic sensitivity, weather-related production uncertainty, and evolving geopolitical trade dynamics. Soybeans weakened amid uncertainty surrounding U.S.–China agricultural commitments, Cocoa remained structurally supported by persistent supply-side concerns and climate-related risks, while Raw Cashew Nuts continued to benefit from resilient Asian procurement demand and comparatively firm physical market fundamentals. Looking ahead, market direction is expected to remain highly dependent on weather developments, trade negotiations, freight conditions, and broader global demand trends across key agricultural import markets.