Global agricultural commodities markets closed the week on a mixed but increasingly volatile note, as market participants reacted to evolving geopolitical developments, trade policy uncertainty, tightening supply conditions, and persistent weather-related production risks across key agricultural producing regions. Trading activity remained concentrated within Soybeans, Cocoa, and Raw Cashew Nuts (RCN), with investors and physical market participants closely monitoring developments capable of reshaping global trade flows, procurement behaviour, and medium-term supply availability.

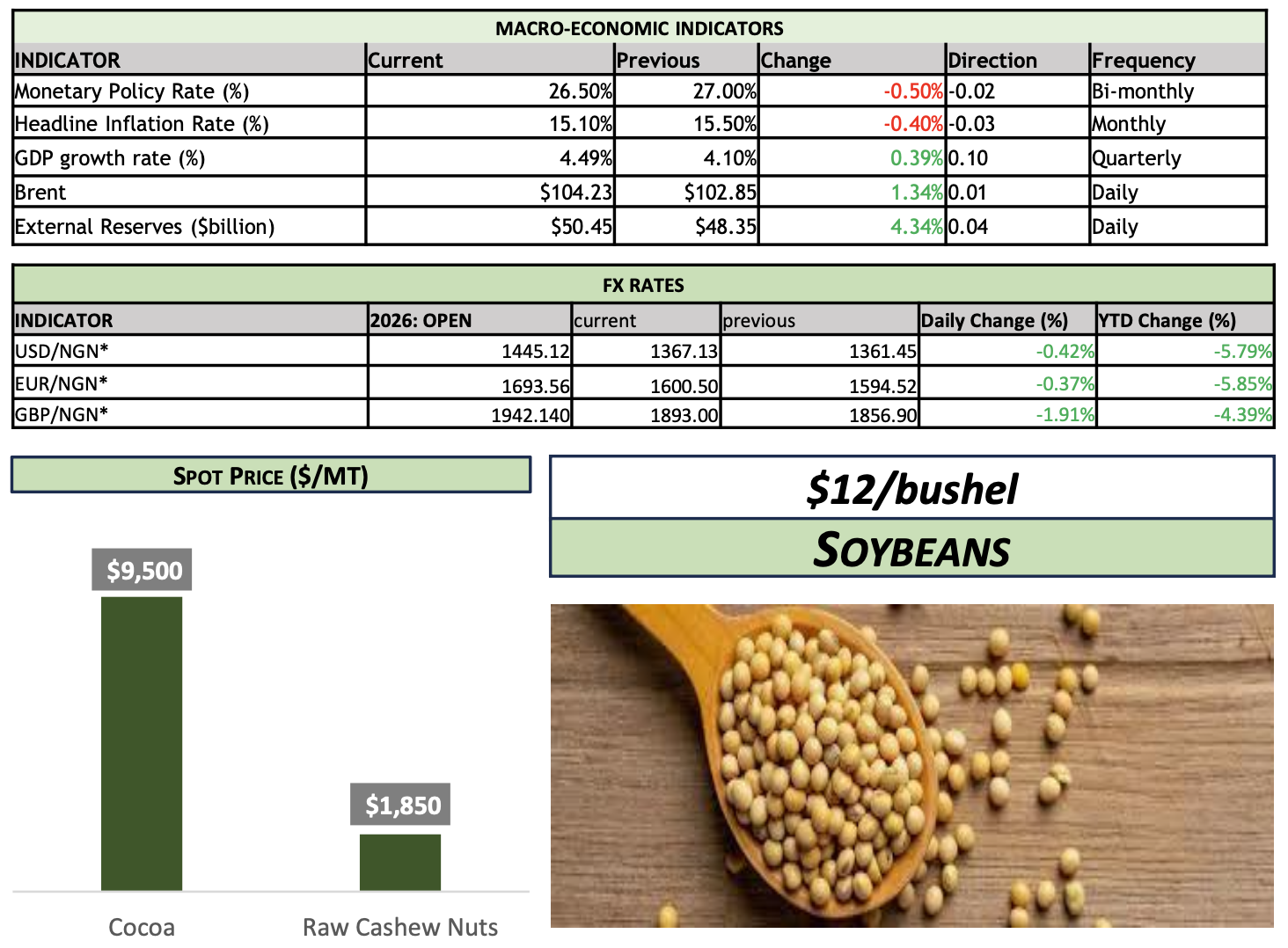

Soybean markets weakened during the week, with benchmark prices retreating toward the $12/bushel level after recently reaching two-year highs. Market sentiment softened following uncertainty surrounding the proposed U.S.–China agricultural trade framework, particularly after Chinese authorities declined to confirm the Trump administration’s assertion that Beijing would commit to purchasing at least $17 billion annually in U.S. agricultural products through 2028. Prices had initially rallied earlier in the week after announcements surrounding high-level discussions between President Donald Trump and President Xi Jinping raised expectations of stronger Chinese agricultural demand. However, momentum reversed after China’s Ministry of Commerce clarified that both countries had only agreed on a broader “guiding target” aimed at increasing agricultural trade volumes without confirming specific purchase commitments.

Despite the correction, underlying soybean market fundamentals remained relatively supported by resilient global feed demand and tightening U.S. stock projections. Nevertheless, producers continued to face mounting pressure from subdued crop margins, elevated production costs, tariff- related uncertainties, and rising fertilizer prices linked to geopolitical tensions in the Middle East. Additionally, Brazil continued to remain a major competitive force within global soybean trade flows, with market participants closely monitoring the potential rerouting of export volumes should U.S.–China agricultural trade commitments materialize further in the coming months.

Within the soft commodities segment, Cocoa markets remained highly sensitive to supply-side developments and weather-related risks across West Africa. Cocoa prices continued to consolidate after the sharp volatility witnessed earlier in the year, with Trading Economics data showing futures easing below the $4,200/MT level despite broader structural concerns remaining supportive. Market participants continued to monitor irregular rainfall patterns across Côte d’Ivoire and Ghana alongside increasing concerns surrounding the possible return of El Niño-linked weather disruptions in the coming production cycle.

However, sentiment within the cocoa market remained mixed following reports that Côte d’Ivoire expects cocoa production to rise by approximately 10.5% during the 2025/26 season, potentially reaching between 2.0–2.1 million metric tons, marking the first production increase in three seasons. The anticipated recovery has largely been attributed to stronger farmer investment in fertilizers and improved plantation management following elevated cocoa prices over recent years. Nevertheless, concerns surrounding drought conditions, weak flowering rates, and long- term climate-related risks continued to limit broader bearish positioning across the cocoa market.

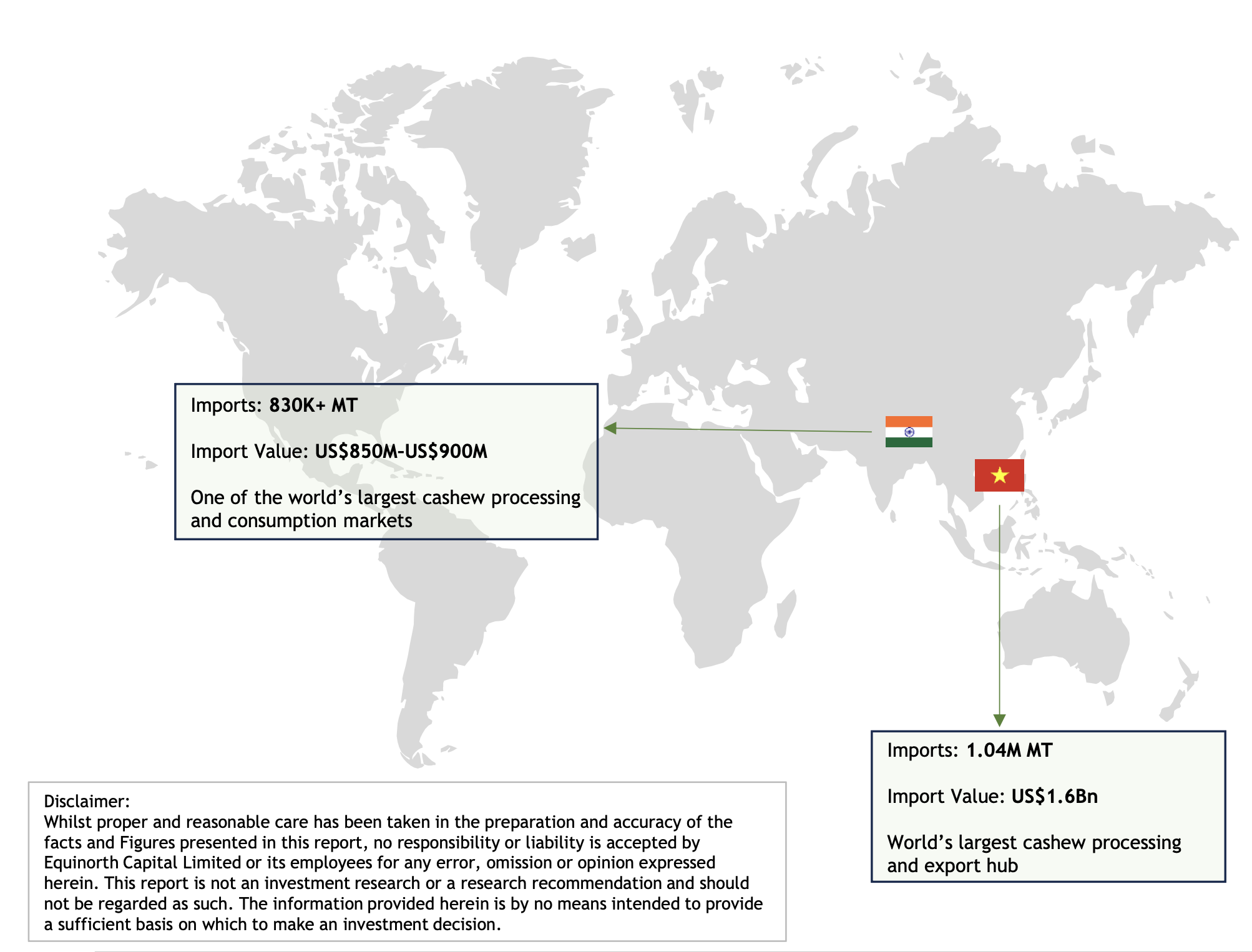

Raw Cashew Nut (RCN) markets maintained a relatively firm structure during the review period, supported by stable procurement activity from key Asian processing markets and comparatively tight supply availability across West African producing regions. Export demand from India and Vietnam remained supportive of pricing sentiment, while elevated inland logistics costs, shipment delays, and currency fluctuations continued to influence transaction activity and procurement behaviour across physical trading channels. Although broader liquidity conditions remained moderate, underlying demand fundamentals across the cashew segment remained comparatively resilient amid steady global consumption trends.

Across the broader agricultural commodities landscape, market sentiment remained heavily influenced by freight market volatility, inflationary pressures, weather developments, geopolitical tensions, and uncertainty surrounding global trade negotiations. Participants continued to monitor developments capable of impacting supply chains, export competitiveness, financing conditions, and physical commodity flows across major producing and consuming regions.

Overall, the week reflected heightened sensitivity across agricultural commodity markets as investors reacted to evolving geopolitical signals, weather-related production concerns, and shifting trade expectations. Soybeans experienced corrective pressure tied to uncertainty surrounding U.S.–China agricultural commitments, Cocoa remained structurally supported amid persistent supply risks and El Niño-related weather concerns despite improving production forecasts from Côte d’Ivoire, while Raw Cashew Nuts continued to benefit from resilient Asian procurement demand and relatively firm physical market fundamentals. Looking ahead, market participants are expected to remain focused on weather developments, trade negotiations, export demand trends, and broader macroeconomic conditions as key drivers likely to shape agricultural commodity pricing and market sentiment in the near term.

Source – Tradingeconomics