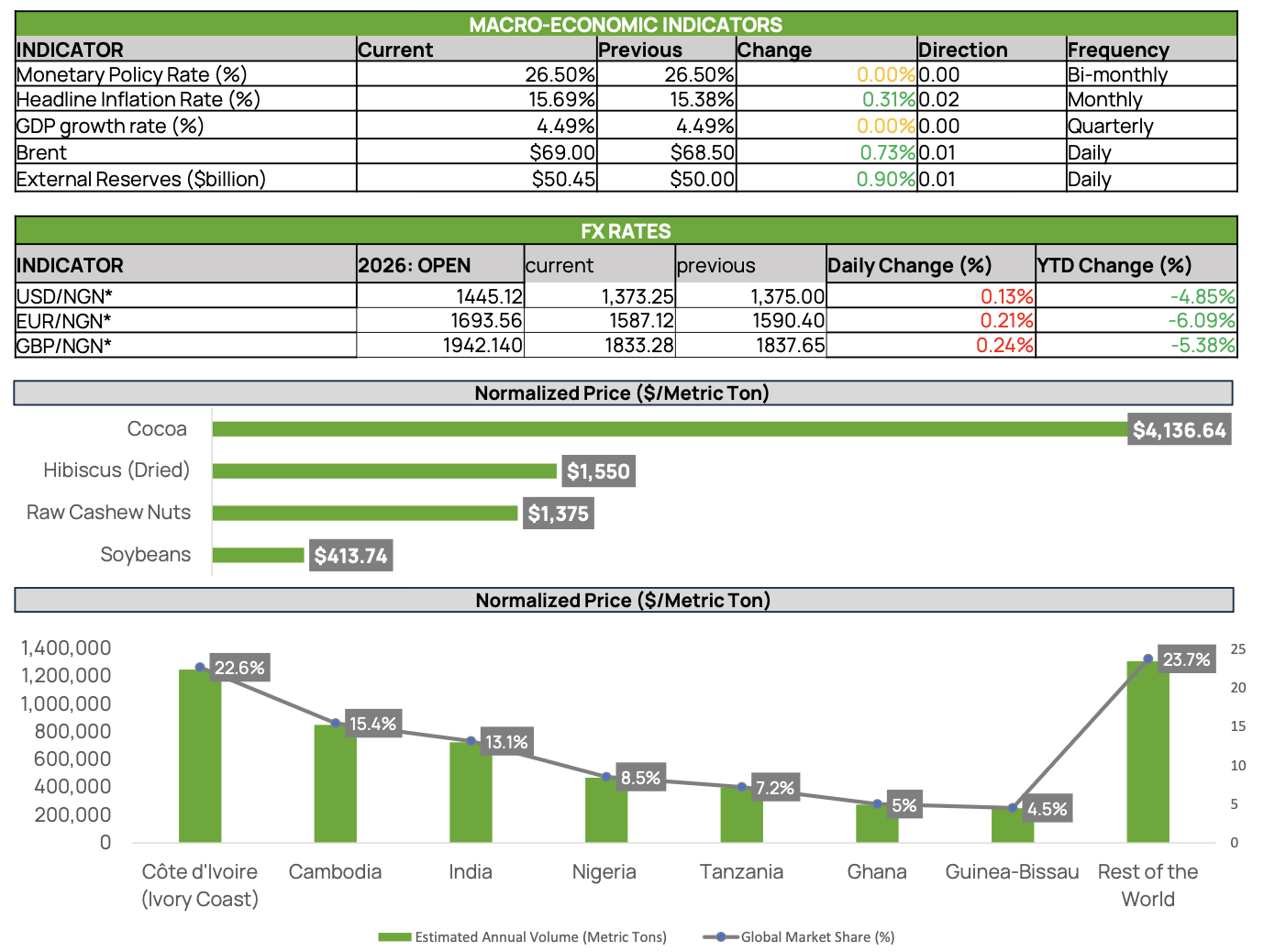

Global agricultural commodity markets closed the week with diverging fundamentals across major export-oriented commodities, as improving crop conditions in North America contrasted with persistent weather concerns in West Africa. Market participants remained focused on supply outlooks, inventory developments, and procurement activity across key consuming regions, with sentiment increasingly shaped by expectations for the current production cycle.

The soybean market experienced notable pressure during the week as improving weather conditions across major U.S. growing regions strengthened expectations of a well-supplied market. Favorable rainfall across key producing states eased earlier drought concerns, while planting progress continued at an accelerated pace. According to recent USDA data, soybean planting reached 87% completion by late May, ahead of the historical average, while crop emergence also exceeded normal seasonal levels. These developments reinforced expectations of a potentially strong harvest and increased near-term supply availability.

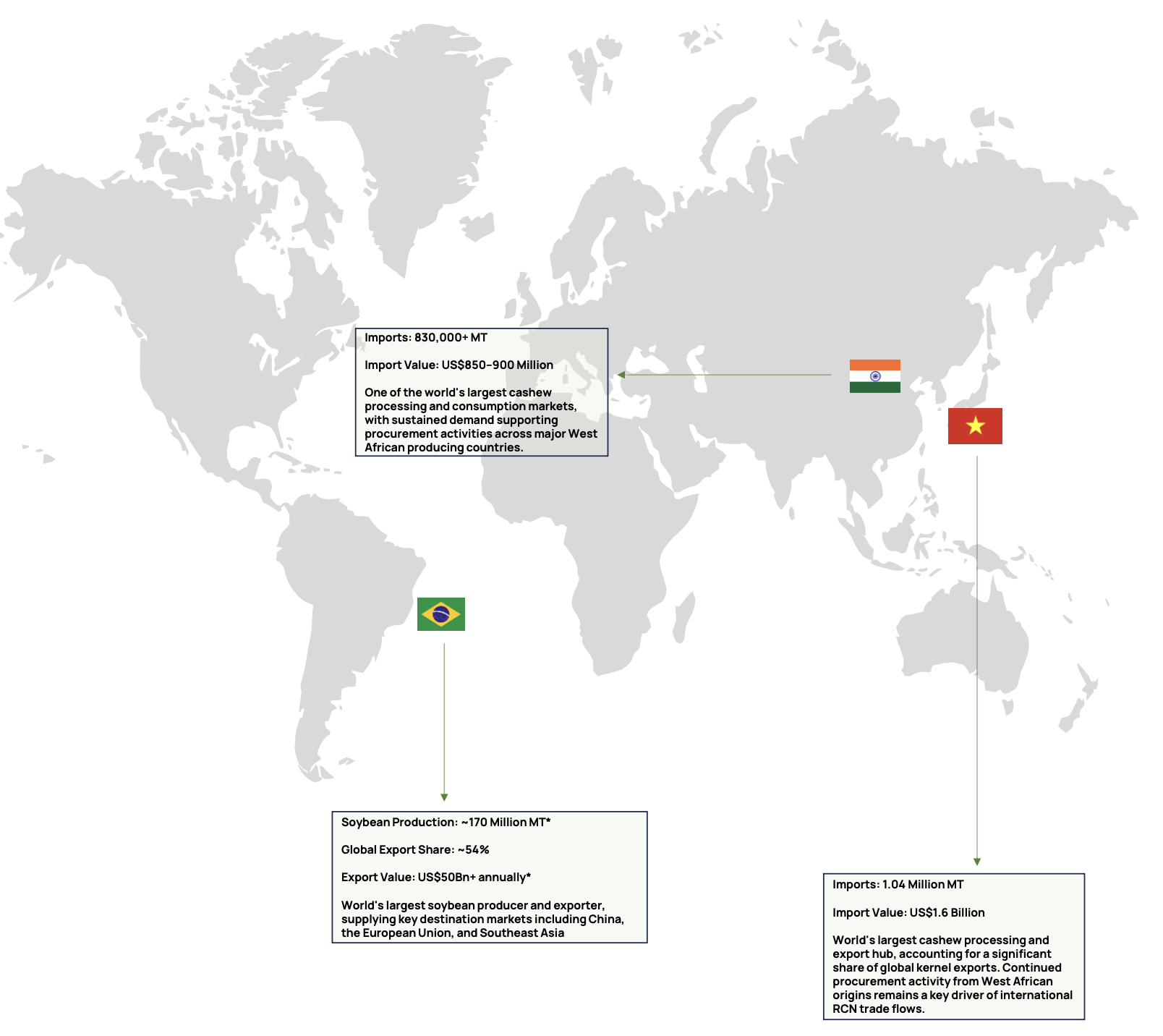

Beyond weather conditions, export demand remained a key area of focus. While China continues to represent the most significant destination for global soybean trade, purchasing activity has remained inconsistent in recent months. Nevertheless, reports indicating that Chinese buyers have begun placing orders for the 2026 crop provided some support to longer- term demand expectations. For physical market participants, the combination of improving supply prospects and uncertain export demand continues to place downward pressure on spot soybean indications across major export origins, particularly in North and South America.

Within the cocoa market, attention remained firmly fixed on the balance between supply recovery expectations and ongoing weather-related risks. Although cocoa prices have recovered from recent lows, market participants continue to assess the potential impact of weather developments across Côte d’Ivoire and Ghana, which collectively account for more than 60% of global cocoa production. The possibility of renewed weather disruptions associated with the El Niño climate cycle remains a key concern, particularly given the market’s recent experience with lower yields and reduced bean quality across major producing regions.

At the same time, emerging signs of improved supply conditions limited stronger upward price momentum. Farmers across several cocoa-growing regions in Côte d’Ivoire reported rainfall levels sufficient to support the ongoing mid-crop, contributing to expectations of improved production during the 2025/26 season. Market sentiment was further influenced by rising global inventories, with cocoa stocks reaching their highest levels in nearly two years. The increase in available inventories has provided some reassurance to processors and buyers following a prolonged period of supply tightness and exceptional price volatility.

Raw Cashew Nut (RCN) markets have demonstrated notable price stability, decoupling from the heightened volatility observed across broader commodity complexes. This stability is primarily driven by physical supply chain fundamentals, structural export demand, and processing capacity utilization rather than speculative positioning. By shrugging off the macro-driven fluctuations seen in commodities markets, the physical cashew trade continues to be dictated by real-time industrial requirements and immediate supply chain execution.

From a trade perspective, Vietnam and India continue to dominate global raw cashew procurement activity, firmly reinforcing their positions as the principal demand hubs within the international cashew value chain. This sustained procurement activity from Asia’s dominant processing centers provides a critical floor for the market, continually underpinning trade flows from key West African origin markets. Importers and processors in these destination hubs are actively prioritizing risk mitigation, focused heavily on maintaining robust forward inventory coverage to secure necessary raw materials well ahead of future production cycles and to fulfill strict near- term export commitments.

However, navigating this market requires a sophisticated understanding of broader operational and macroeconomic friction points. Market participants remain highly attentive to fluctuating logistics and freight costs, tightening warehouse financing conditions, and volatile currency movements. Each of these variables plays a critical role in micro-level execution, directly influencing localized transaction pricing and altering procurement strategies across various origin markets.

Looking ahead, global market attention is expected to remain tightly focused on three critical, interconnected themes: improving crop prospects across the U.S. soybean belt, shifting weather developments across West African cocoa-producing regions, and the ongoing velocity of procurement activity among Asian cashew processors. Together, this matrix of agricultural and macroeconomic factors is poised to heavily shape international commodity trade flows, dictate corporate inventory management decisions, and drive spot market pricing dynamics throughout the coming weeks.